Establishing The Printing House of the World at Light Speed

Why the AI Economy Has Already Decided Who Wins, and What the Rest of Us Are Actually Building

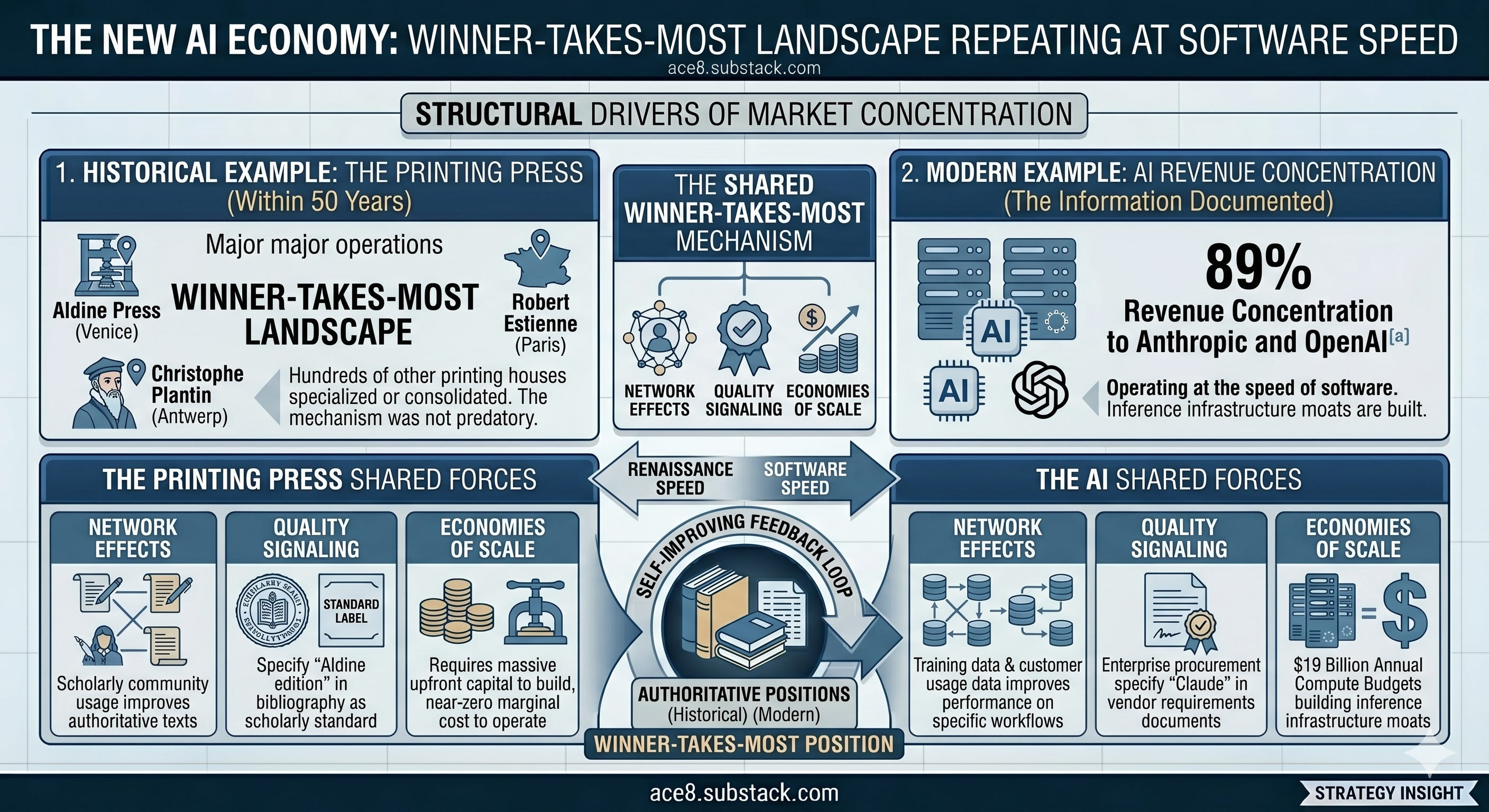

In 1501, Aldus Manutius held the only press in Europe printing authoritative Greek texts. According to The Information, In 2026, Anthropic and OpenAI hold the only inference infrastructure generating 89% of all AI revenue. The question we examine is what the scribes in the remaining 11% are actually making — and whether it compounds.

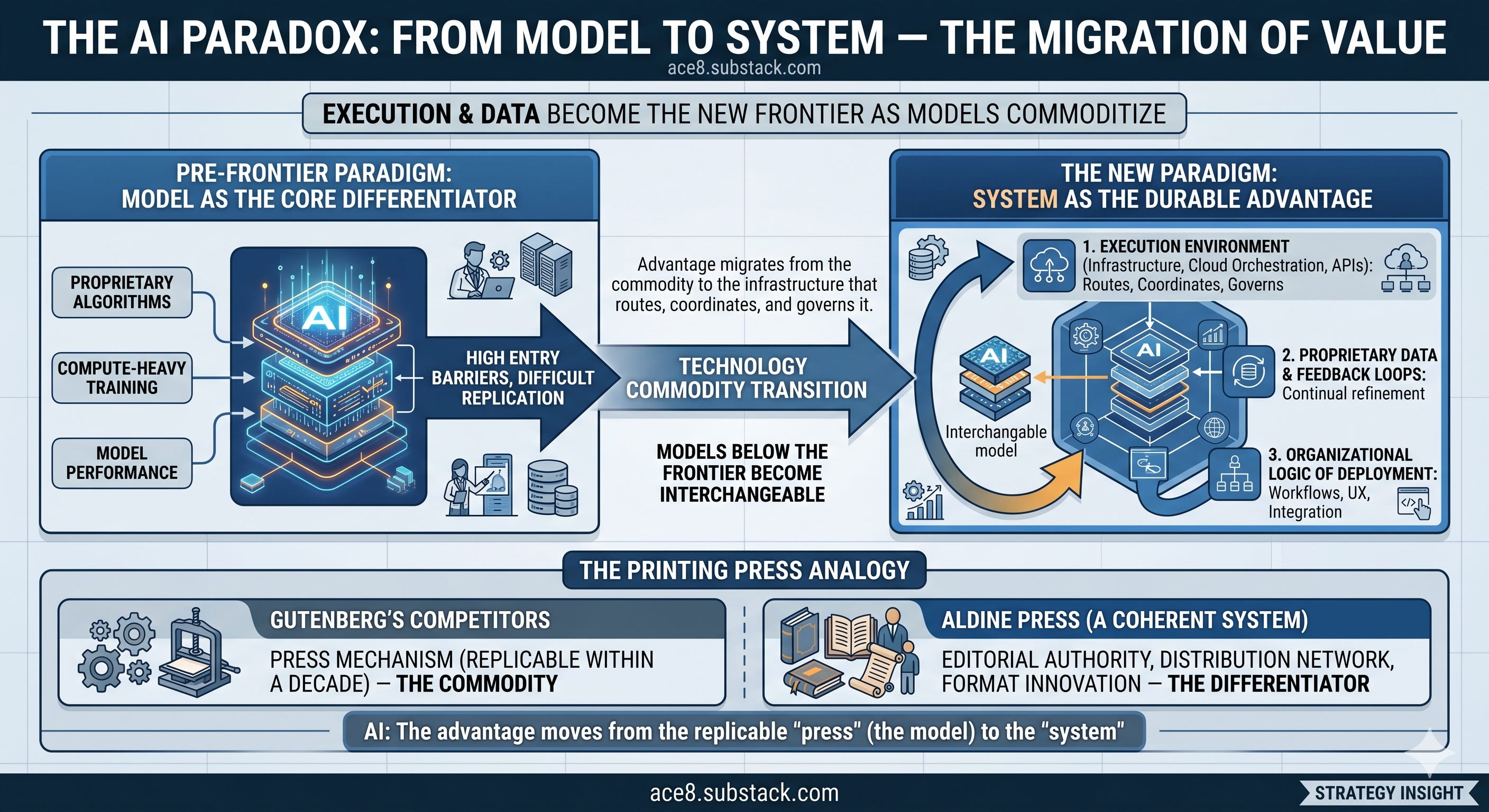

In 1501, Aldus Manutius completed the first volume of his pocket-sized octavo edition of Virgil — a book small enough to fit in a coat pocket, priced to reach not just the wealthy patron but the traveling scholar, the merchant’s educated son, the university student who could not afford a folio. The Aldine Press had spent the previous seven years printing authoritative editions of Greek and Latin classics in formats and at prices that no previous printing operation had attempted. By 1501, it had become, functionally, the infrastructure layer of European intellectual life — the institution whose imprimatur determined which texts were authoritative, whose typefaces became the standard, whose dolphin-and-anchor colophon served as the quality signal that the entire market navigated by.

Aldus invented the operating system on top of the printing press: the editorial standards, the distribution model, the format innovation, and the network of scholars whose participation converted raw printing capacity into cultural authority. The other printing houses of Venice — and there were dozens — continued to operate. Some of them printed good books. None of them printed the books that defined the century.

There is no infrastructure-independent personal OS. The question is whose infrastructure dependency you are choosing, at what price point, under what geopolitical risk architecture.

The Information’s recent reporting that Anthropic and OpenAI together account for 89% of all AI revenue in 2026 is the Aldine Press moment rendered in balance sheets. The other printing houses are still running. The question of whether anything running in the remaining 11% constitutes a durable position — or whether it is, at best, a specialized workshop operating on the sufferance of the infrastructure it depends on — is the question that the current discourse about personal AI operating systems, agentic orchestration platforms, and open-source model economics has not yet found the courage to answer directly.

Analyzing Anthropic’s Revenue Architecture

The revenue numbers, assembled accurately, are more concentrated than any comparable technology transition in the past thirty years.

Anthropic reached a $30 billion annualized revenue run rate in April 2026, having grown from $1 billion in December 2024 to $9 billion at the end of 2025 to $19 billion in March and $30 billion in April — $11 billion added in a single month, a growth rate that has no historical precedent in enterprise software. Over 1,000 business customers now each spend more than $1 million annually with Anthropic, a figure that doubled in less than two months. 80% of Anthropic’s revenue comes from enterprises. It is currently valued at between $380 billion and $900 billion depending on which funding round one references, projecting $55 billion in 2027 revenue, and not expected to reach cash flow positivity until 2028 — because it is spending approximately $19 billion annually on training and inference compute while generating approximately $19 billion in revenue, a gross margin structure that resembles a railroad more than a software company.

OpenAI sits at approximately $24–25 billion in annualized revenue as of April 2026, having reached $2 billion per month in direct sales. Microsoft generated $30 billion in OpenAI-related revenue between 2023 and 2025 — more than double its $13 billion investment — with OpenAI paying approximately $23 billion in Azure compute fees in that period, meaning that Microsoft’s primary profit center from its OpenAI relationship has been its own cloud infrastructure rather than model resale. The renegotiated terms cap Microsoft’s total OpenAI revenue share at $38 billion through 2030, down from a previous arrangement that could have produced $135 billion in cumulative payments; in exchange, OpenAI gained the right to distribute its models through AWS, Google Cloud, and Oracle, ending Microsoft’s exclusivity. OpenAI will pay approximately $6 billion of its estimated $30 billion in 2026 revenue to Microsoft under the new terms.

Together, these two companies are generating approximately $55 billion in annualized AI revenue at a moment when the entire AI industry’s revenue is being reported as approximately $60 billion. The remaining 11% is not nothing — it includes enterprise deployments, open-source infrastructure companies, specialized vertical AI applications, and the nascent personal AI OS layer. But the concentration is structural, not accidental, and it is tightening rather than relaxing.

The Cost Floor Has Just Been Moved: DeepSeek and What It Actually Means

Into this revenue architecture, DeepSeek V4 arrived in late April 2026 as a two-tier open-weight system — a 1.6 trillion parameter Pro model and a 284 billion parameter Flash variant — both supporting a one million token context window, both carrying an MIT license, both priced at a level that cut the cost floor of generative coding infrastructure by approximately 89% in a single release. DeepSeek V4 Flash is priced at $0.14 per million input tokens and $0.28 per million output tokens. The Pro variant, currently at a 75% discount through May 31, carries an effective rate that places sophisticated frontier-adjacent coding capability at a price point that was, eighteen months ago, associated with commodity text completion, not advanced reasoning.

The developer community’s response was immediate: DeepSeek V4 is already being described as the backend engine of choice for token-hungry agentic workflows — long-context review cycles, parallel agent exploration, bulk codebase indexing — where the difference between a $0.14 and a $3 input token rate determines whether the economic model of an agent-first company closes or doesn’t. The teams extracting maximum leverage from V4 are not replacing their Anthropic or OpenAI frontier models; they are stratifying their inference stack, routing cost-sensitive high-volume workloads to DeepSeek and precision-critical judgment calls to Claude or GPT. The effect is a tiered supply chain for cognition, and DeepSeek has established itself as the rare earth refinery of that supply chain — the cost infrastructure layer that makes the entire stack cheaper without displacing the premium instrument at the top.

The deeper implication, which the developer community has begun to articulate with increasing precision, is that if models are becoming interchangeable below the frontier, then the durable advantage in the AI economy does not sit in the model. It sits in the execution environment, the data, and the organizational logic of how the model is deployed. This is the same conclusion that every technology commodity transition eventually produces: the advantage migrates from the commodity to the infrastructure that routes, coordinates, and governs it. In the printing press analogy, the advantage migrated from the press mechanism — which Gutenberg’s competitors could replicate within a decade — to the editorial authority, distribution network, and format innovation that only the Aldine Press had built into a coherent system.

The Pricing Signal: From Flat Rate to Token Retail

The dolphin-and-anchor colophon told the market: this text is trustworthy. The market that emerges on the other side of the AI transition will need a different colophon — one that tells it not that the text is fast and fluent, but that the judgment behind it is sound.

Anthropic’s 2026 pricing evolution is the most strategically significant signal in the current market, and it has received less analytical attention than the revenue headline numbers deserve.

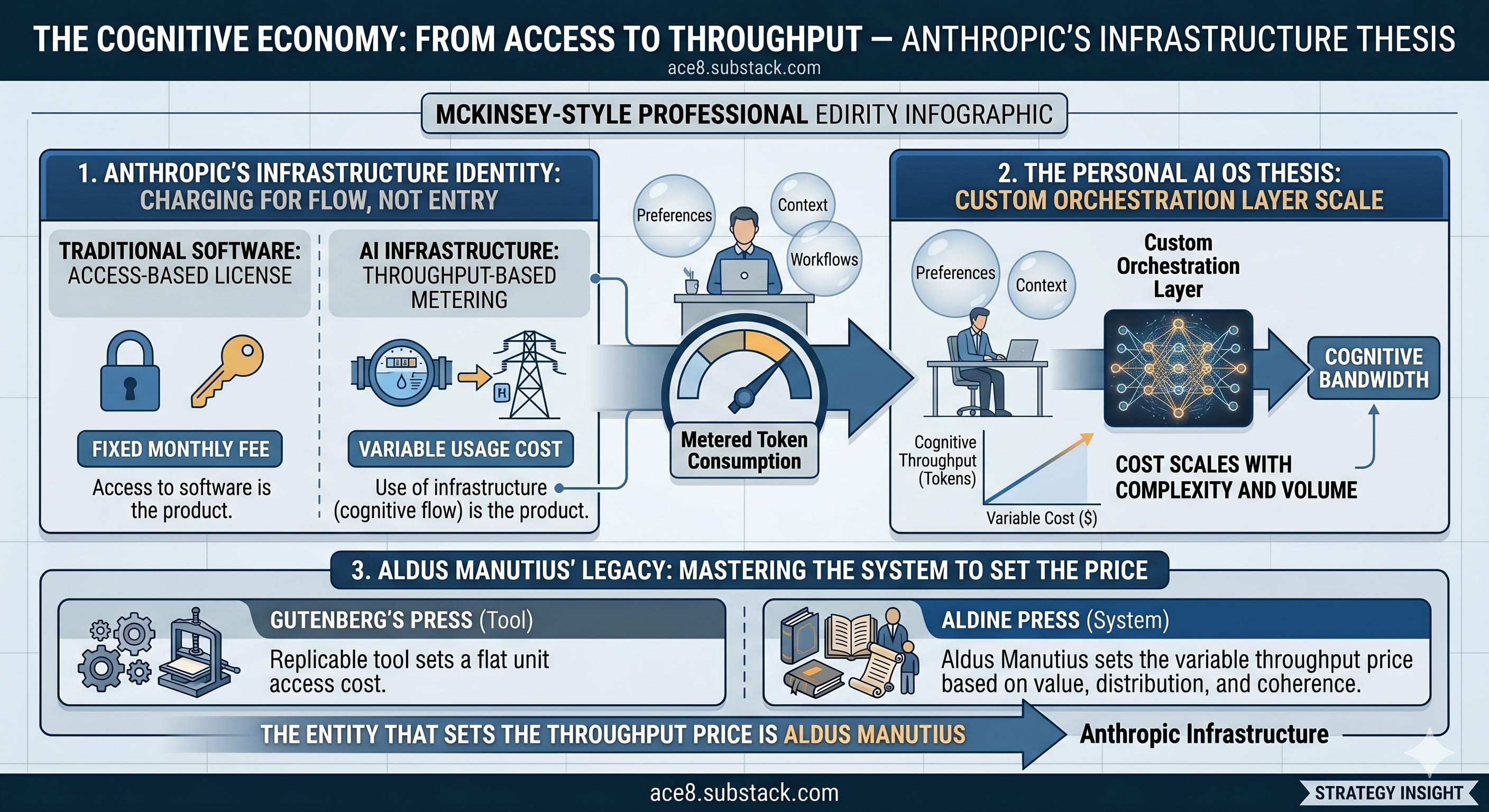

The Max subscription plans — originally priced as flat-rate unlimited bundles designed to build user adoption — are under visible pressure. A/B testing observed across accounts in April 2026 showed the Max-20 plan being presented at both $200 and $300 per month to different users in the same geography, a classic pre-hike testing pattern. Separately, Anthropic eliminated long-context surcharges as of March 13, standardizing per-token pricing across context lengths — a simplification that makes the API’s cost architecture more legible and more predictable for enterprise procurement, which is a signal about where the company believes its durable revenue base sits.

The direction is clear: Anthropic is migrating from the consumer SaaS flat-rate model — which transfers compute cost risk from user to vendor in a way that becomes unsustainable as usage intensity grows — toward token retail pricing that reflects actual inference economics.

Anthropic is an infrastructure company that happens to have a consumer interface, and infrastructure companies charge for throughput, not for access. The implication for the personal AI OS thesis — the idea that every individual will soon run a custom orchestration layer tuned to their own context, preferences, and workflows — is that the cost of that OS is not a fixed software license. It is a variable infrastructure cost that scales with cognitive throughput, and the entity that sets the throughput price is Aldus Manutius.

The Personal OS Layer: Post-Prompt, Post-Agentic, Pre-Reckoning

The AI revenue concentration is the same mechanism operating at the speed of software rather than the speed of the Renaissance.

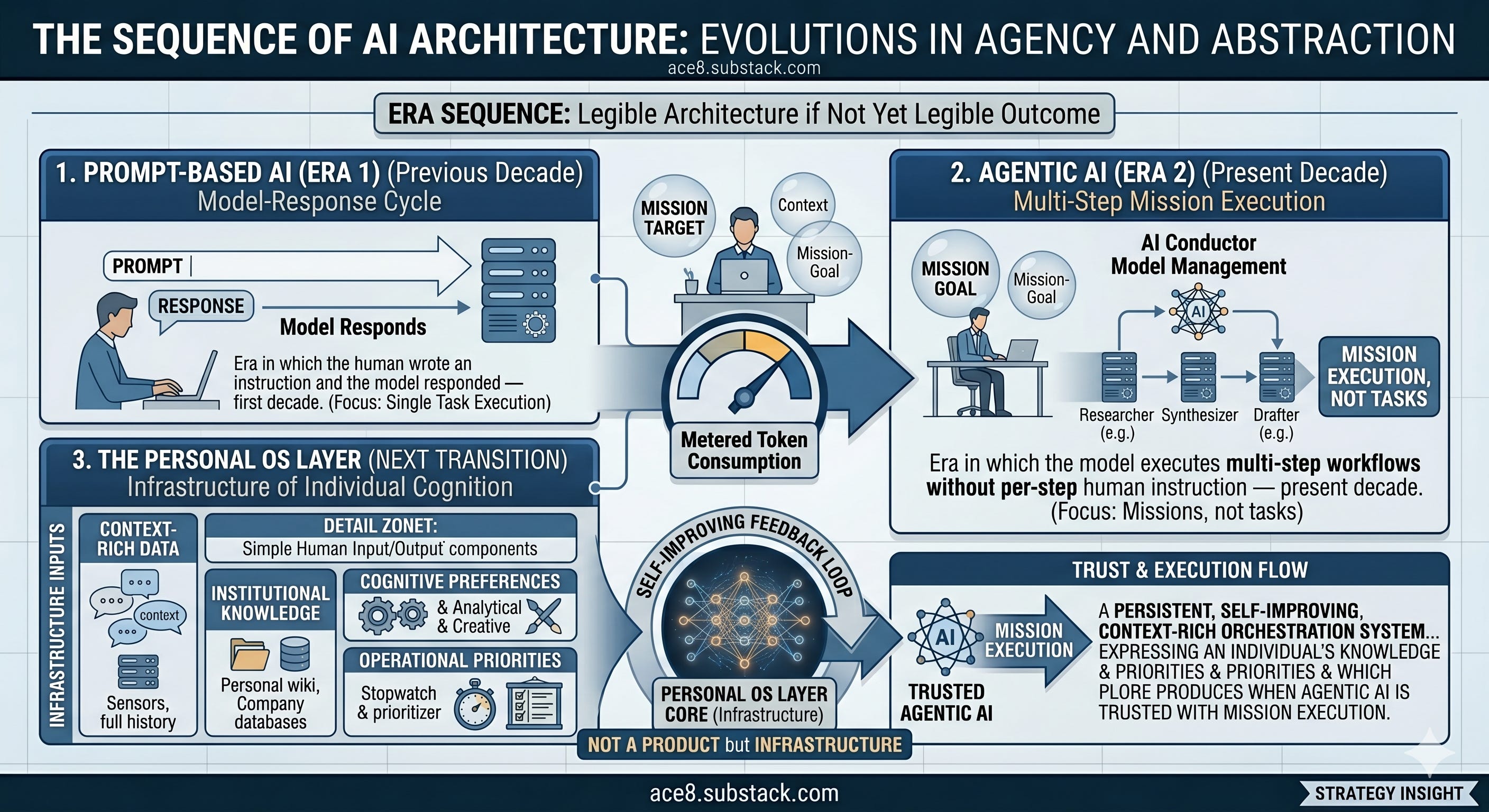

The sequence is now legible in its architecture if not yet in its outcome. Prompt-based AI — the era in which the human wrote an instruction and the model responded — was the first decade. Agentic AI — the era in which the model executes multi-step workflows without per-step human instruction — is the present decade. The personal OS layer — a persistent, self-improving, context-rich orchestration system that is not a product but an infrastructure that expresses a specific individual’s cognitive preferences, institutional knowledge, and operational priorities — is what the next transition produces when agentic AI is sufficiently mature to be trusted with the execution of a mission rather than a task.

Platforms like Paperclip, gstack, and Hermes are the early commercial expressions of this layer. Paperclip’s “human control plane for AI labor” is the governance architecture of a personal OS: the org chart, the mission, the budget, the audit log. gstack’s insight — that the leverage is in the operating system beneath the agent, not in the proliferation of agents — is the architectural principle of the personal OS stated from the engineering side. Hermes’s self-improving, self-hosted, model-agnostic design is the privacy-sovereign expression of the personal OS: the system that runs inside your security perimeter, learns your context over time, and builds skills tuned to your specific operational reality.

The cost architecture of this layer, however, is not what its advocates typically describe. It is not a fixed-cost alternative to enterprise software licenses. It is a variable-cost inference infrastructure whose floor is set by DeepSeek’s commodity pricing, whose ceiling is set by Anthropic’s token retail rates, and whose total cost of ownership includes the supply chain risks that the analysis of rare earth dependencies and BRI mineral corridors has already established as the material substructure of every advanced computing platform in the world.

Building a personal OS on Anthropic’s API means building a personal OS whose operational continuity depends on Anthropic’s token pricing decisions, Anthropic’s API availability, and the CHIPS supply chain that delivers the H100 clusters on which Anthropic’s inference runs. Building it on a self-hosted DeepSeek deployment means building it on a model whose training compute ran through Chinese infrastructure and whose continued development is subject to the same geopolitical architecture that Xi Jinping was describing, in a different register, when he invoked the Thucydides Trap at the Beijing summit.

There is no infrastructure-independent personal OS. The question is whose infrastructure dependency you are choosing, at what price point, under what geopolitical risk architecture.

The Winner-Takes-All Geometry

Personal OS platforms compound to the extent that they build irreplaceable user context that makes switching costs prohibitive regardless of which foundation model runs underneath.

The printing press produced, within fifty years of its invention, a winner-takes-most landscape: the Aldine Press, Christophe Plantin’s Antwerp operation, and Robert Estienne’s Paris workshop held the authoritative positions in their respective categories, and the hundreds of other printing houses either specialized into sustainable niches or consolidated into those operations’ supply chains. The mechanism was not predatory. It was the natural operation of network effects, quality signaling, and the economies of scale inherent in any infrastructure that requires massive upfront capital to build and near-zero marginal cost to operate at the frontier.

The AI revenue concentration is the same mechanism operating at the speed of software rather than the speed of the Renaissance. The network effects are the model’s training data and the enterprise customers whose usage data improves the model’s performance on their specific workflows. The quality signal is the anthropic colophon: the enterprise procurement officer who specifies “Claude” in the vendor requirements document is performing the same function as the scholar who specified “Aldine edition” in the bibliography. The economies of scale are the $19 billion annual compute budgets that only two organizations in the world currently operate at, building inference infrastructure moats that no VC-funded challenger can replicate within the current capital cycle.

The remaining 11% of the AI economy occupies four distinct positions in this geometry. Specialized vertical applications — the healthcare AI, the legal AI, the financial modeling AI — compound because their value is in the domain-specific training data and the workflow integration, neither of which the foundation model vendors can easily replicate without becoming their customers’ competitors.

Open-source infrastructure companies — the Hugging Face layer, the inference optimization tools, the fine-tuning platforms — compound because they are the supply chain for the 89%, not its competitors. Personal OS platforms compound to the extent that they build irreplaceable user context that makes switching costs prohibitive regardless of which foundation model runs underneath. What does not compound, in this geometry, is the undifferentiated AI application company whose value proposition is “we use Claude to do X” without an asset — a dataset, a workflow integration, a user context layer, a domain network — that is not replicable by Anthropic building the same application themselves.

China’s position in this geometry requires its own accounting, because it operates outside the competitive logic of the Western AI market rather than inside it. DeepSeek’s V4 is not competing with Anthropic for the same enterprise contracts. It is establishing the cost floor of the global inference commodity market from a position of structural independence from the rare earth supply chain constraints, the CHIPS Act restrictions, and the dollar-denominated capital markets that constrain every Western AI company’s build rate. The Silk Road initiative’s mineral corridors and the BRI’s infrastructure network are, in the AI economy, the equivalent of owning the paper mills and the type foundries: the upstream inputs that determine the cost structure of everything printed on the press. China does not need to win the foundation model race to win the AI economy. It needs only to control the cost floor of the commodity layer and the supply chain inputs of the premium layer — which it already does, in the form of rare earth processing dominance and the manufacturing infrastructure that produces the GPUs on which every model, including Anthropic’s, ultimately runs.

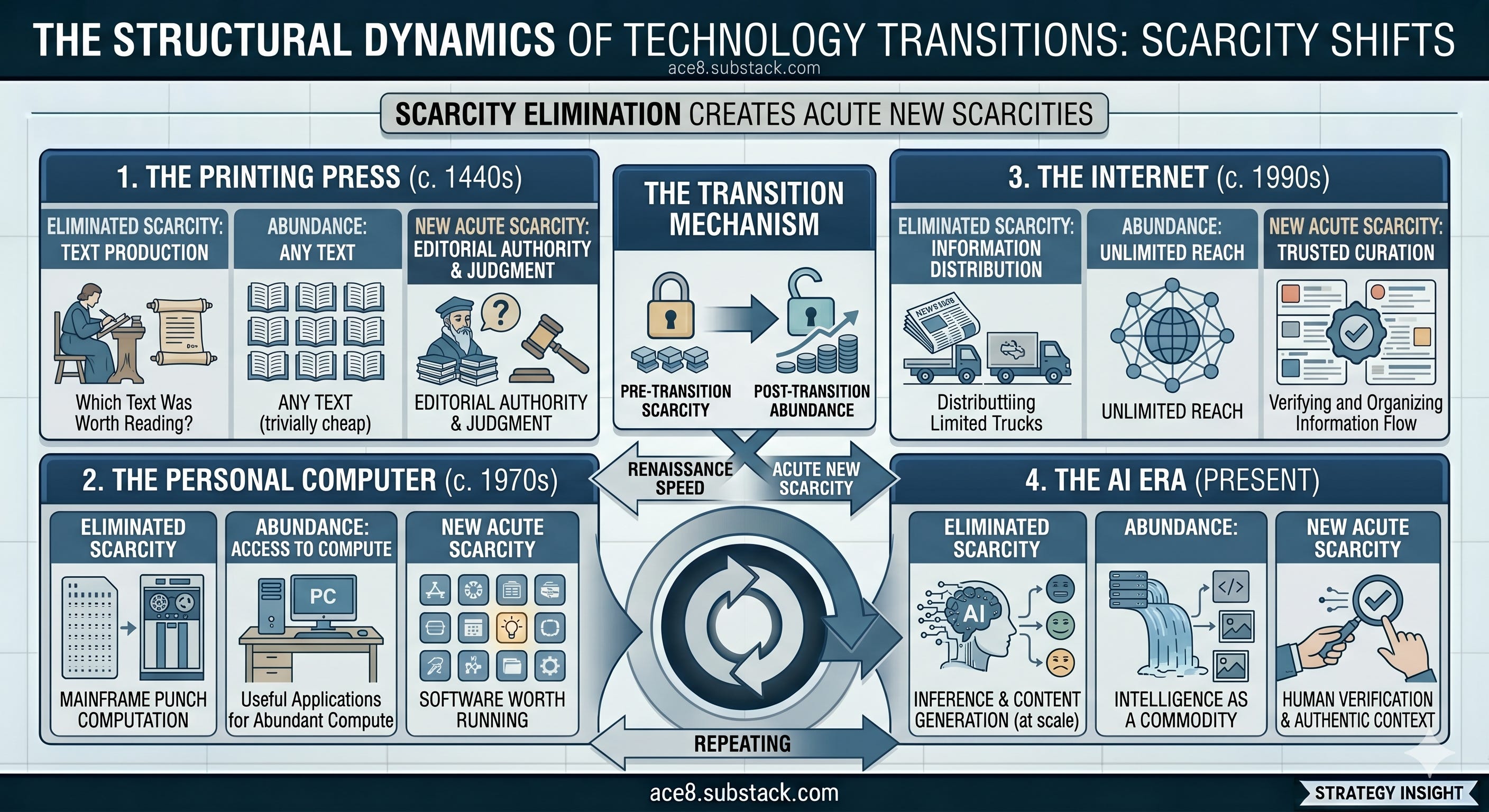

The Scarcity That Remains

It is a structural feature of every technology transition that the elimination of one form of scarcity creates, as a byproduct, a more acute form of a different scarcity. The printing press eliminated the scarcity of text production and created, in its place, an acute scarcity of editorial authority — the judgment about which text was worth reading in a world where printing anything had become trivially cheap. The personal computer eliminated the scarcity of computation and created an acute scarcity of software that was worth running. The internet eliminated the scarcity of information distribution and created an acute scarcity of trusted curation.

The current transition is eliminating the scarcity of cognitive labor — the execution of analysis, writing, coding, reasoning, and coordination that previously required human time — and creating, in its place, an acute scarcity of institutional wisdom: the judgment about which mission is worth executing, which output is trustworthy, which relationship requires a human to close, and which strategy the agents are currently executing is the wrong strategy with no human in the loop to notice.

This scarcity is not accessible to the 89% that controls the inference infrastructure. It is, structurally, the only asset class that does not sit inside Anthropic’s data center or OpenAI’s model weights. It sits inside the organizations and individuals who have preserved and amplified it through the transition rather than treating it as overhead to be eliminated.

The winner-takes-all geometry of AI revenue concentration is real, documented, and tightening. The Aldine Press held the authoritative position in European intellectual infrastructure for fifty years. Anthropic and OpenAI will hold their analogous position for a duration that the current capital structure and network effects make difficult to dislodge. The question for everyone operating outside the 89% is not how to compete with the printing house of the world. It is what the printing house cannot print — and whether that asset, built carefully and compounded deliberately, is the thing that the century eventually decides it needed most.

The dolphin-and-anchor colophon told the market: this text is trustworthy. The market that emerges on the other side of the AI transition will need a different colophon — one that tells it not that the text is fast and fluent, but that the judgment behind it is sound. That colophon cannot be trained into a model. It has to be earned, in the old way, by the people who stayed in the building and kept doing the work.

Alan Eyzaguirre writes about technology based on decades of experience at the forefront of technology (Apple, Cisco, PayPal), and the humanities (Aspen Institute, Los Angeles County Museum of Art). ace8.substack.com tracks the AI phenomenon through an integrative, Holon-oriented lens in order to make this fast-paced market more accessible to the public.