Examining Prediction Markets, Ethics, and AI

Prediction markets, blockchain settlement, and the need for better indicators

Hunter S. Thompson, writing about the television business in Generation of Swine, produced one of the more durable sentences in American journalism:

“The TV business is a cruel and shallow money trench, a long plastic hallway where thieves and pimps run free, and good men die like dogs. There’s also a negative side.”

The quote has migrated, through decades of misattribution, into the music industry and beyond, because the structure of the observation is infinitely portable. Every industry that sits at the intersection of technology, capital, and human desire for fast answers eventually earns it.

Crypto has earned it several times over. And yet, inside that long plastic hallway, something structurally consequential has appeared: event markets whose prices can, under the right conditions, become serious inputs to climate risk modeling, AI systems, and enterprise decision-making. The executive challenge is not whether to dismiss prediction markets or to celebrate them. It is how to locate the mechanism — calibrated, governed, enforced — that separates the instrument from the noise.

The platform thesis, and what it actually claims

In January 2014, Marc Andreessen published “Why Bitcoin Matters” in The New York Times. The opening paragraph is worth reading carefully, because it frames a pattern rather than a specific technology:

“A mysterious new technology emerges, seemingly out of nowhere, but actually the result of two decades of intense research and development by nearly anonymous researchers. Political idealists project visions of liberation and revolution onto it; establishment elites heap contempt and scorn on it. On the other hand, technologists are transfixed by it. They see within it enormous potential and spend their nights and weekends tinkering with it. Eventually mainstream products, companies and industries emerge to commercialize it; its effects become profound; and later, many people wonder why its powerful promise wasn’t more obvious from the start. What technology am I talking about? Personal computers in 1975, the Internet in 1993, and — I believe — Bitcoin in 2014.”

The argument Andreessen makes is not primarily about Bitcoin as currency. It is about Bitcoin as a solution to what computer scientists call the Byzantine Generals Problem: how to establish trust between otherwise unrelated parties over an untrusted network without a central intermediary. Bitcoin gives two parties a way to transfer a unique piece of digital property such that the transfer is guaranteed, everyone can verify it, and no one can challenge its legitimacy.

By 2026, Andreessen had extended the thesis directly to the intersection of AI and crypto: “I believe this is essentially the grand convergence of AI and crypto that is about to unfold.” His specific claim was that the contemporary internet was built without a native payment layer — the HTTP 402 status code, “Payment Required,” has gone unused for decades — and that AI agents operating autonomously online will require programmable money to function. “AI agents will require funds, and this is already occurring. If you have a claw and want it to make purchases for you, you need to provide it with money in some form.”

The platform thesis, stripped of token speculation, makes a precise engineering claim: that a distributed ledger solving the Byzantine Generals Problem provides a settlement substrate that is more transparent, programmable, and trustless than the opaque batch-clearing operations still in use at many legacy exchanges. The question worth asking is not whether that claim is right in the abstract, but where it is right in practice, and under what governance conditions it becomes legitimate rather than merely clever.

From Lloyd’s to Chicago to Kalshi: the architecture problem

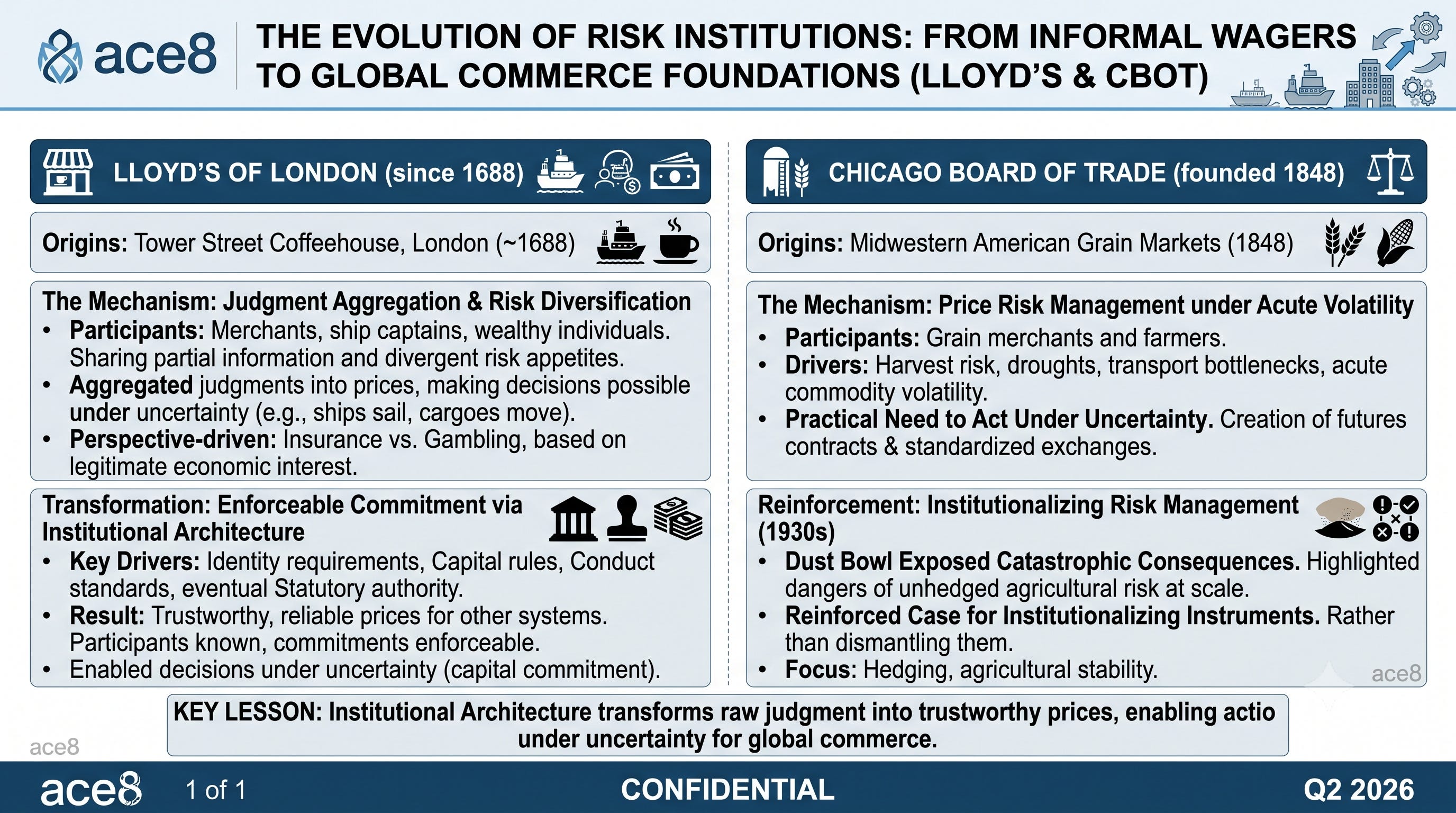

To understand where prediction markets fit in that lineage, it helps to step back from 2026 and look at how structured markets have historically emerged from informal ones.

Lloyd’s began as a coffeehouse on Tower Street in London around 1688, where merchants, ship captains, and wealthy individuals shared information about voyages and made wagers on their outcomes. The underlying mechanism was simple: people with partial information and divergent appetites for risk aggregated their judgments into prices. Those prices made decisions possible under uncertainty. Ships sailed, cargoes moved, capital was committed. Whether this constituted insurance or gambling depended almost entirely on one’s perspective and on whether the participants had a legitimate economic interest in the voyage’s outcome.

What transformed Lloyd’s from an informal gambling ring into the institutional foundation of global maritime commerce was institutional architecture: identity requirements, capital rules, conduct standards, and eventually statutory authority. Prices became trustworthy enough that other systems could rely on them, not because the participants became morally superior, but because their commitments were enforceable and their identities were known.

A structurally similar story sits behind the Chicago Board of Trade, founded in 1848. Grain merchants and farmers in the American Midwest needed a way to express and transfer price risk around harvests in a landscape shaped by drought, transport bottlenecks, and acute commodity volatility. Futures contracts and standardized exchanges emerged not from an abstract commitment to markets, but from the practical need to act under uncertainty. The Dust Bowl of the 1930s, which exposed the catastrophic consequences of unhedged agricultural risk at scale, later reinforced the case for institutionalizing those instruments rather than dismantling them.

The mechanism in both cases: aggregated probabilistic judgment about uncertain events, transformed into prices, enabling economic action that would otherwise have been paralyzed. The transformation over time: not the mechanism, but the architecture surrounding it.

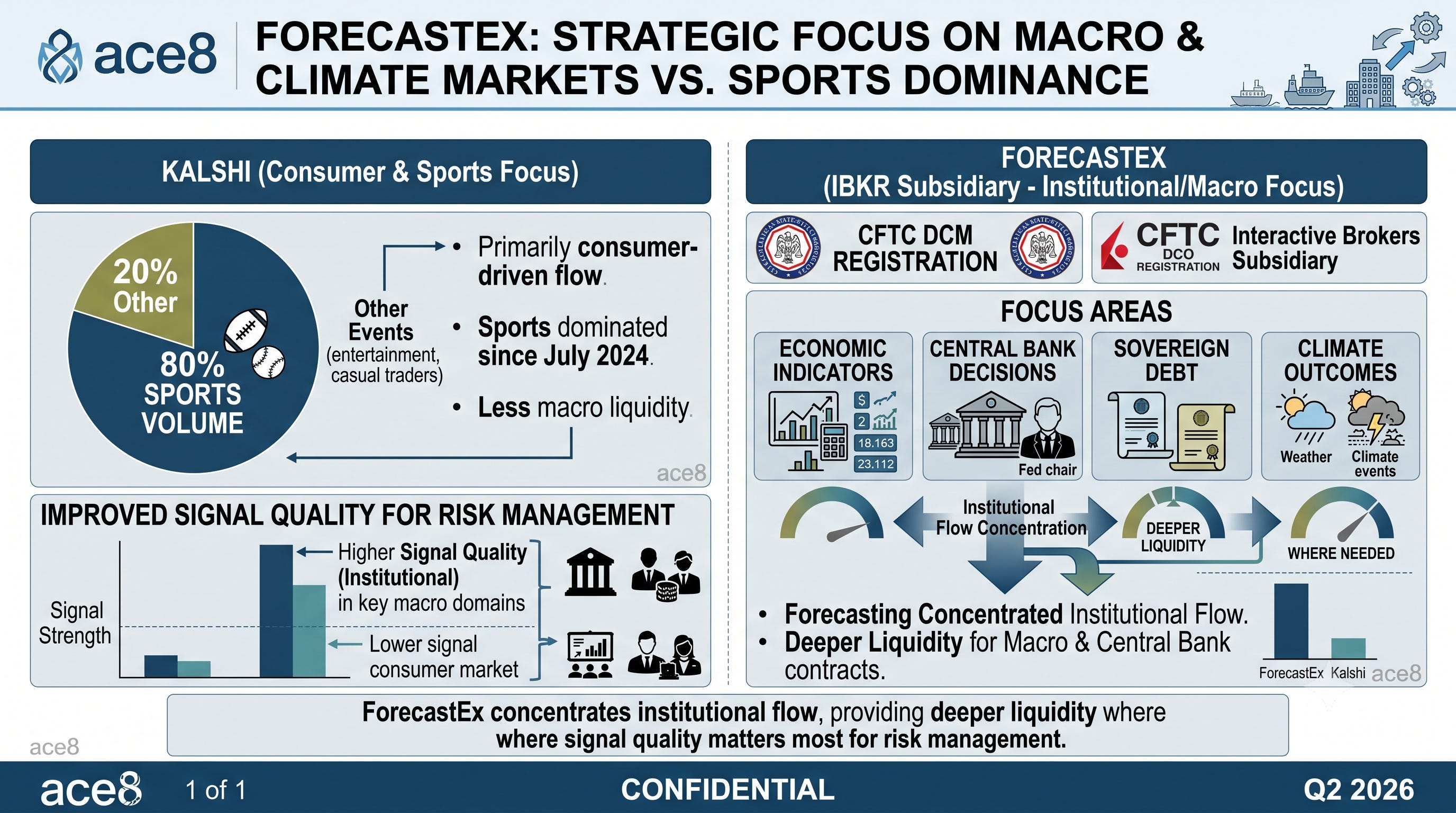

Kalshi sits in that lineage. Founded and approved as a Designated Contract Market by the CFTC in 2020, it became the first fully regulated U.S. prediction market for retail event contracts. A DCM is a specific regulatory status that carries twenty-three Core Principles governing surveillance, financial integrity, anti-manipulation enforcement, and participant protections. When Kalshi lists contracts on congressional elections, sports outcomes, or economic indicators, it does so under the same statutory framework that governs grain and rate futures — not adjacent to it, inside it.

The legal history makes this concrete. When the CFTC tried to block Kalshi’s congressional control contracts, arguing they were contrary to the public interest, the U.S. District Court for the District of Columbia found that the agency had misapplied its own standard. The court held that the term “gaming” did not apply to election contracts and that the contracts did not involve illegal activity under state law. The D.C. Circuit denied an emergency stay. The CFTC eventually dropped the appeal. What changed in that sequence was not the moral status of election trading; it was a legal clarification that event contracts, when properly structured under the Commodity Exchange Act, are financial instruments, not gambling products dressed up in regulatory language.

The February 2026 CFTC enforcement advisory confirmed that the architecture has teeth. Two insider-trading cases were disclosed: one involving a political candidate trading on his own candidacy, another involving a YouTube channel editor trading ahead of content his employer was about to publish — material nonpublic information consumed in a prediction market. Both cases were referred for enforcement. The CFTC made clear that while Kalshi’s internal enforcement program handled the immediate actions, “the Commission has full authority to police illegal trading practices occurring on any DCM, including those described above related to prediction markets.” The enforcement lens reaches through the market into participant conduct. That is the operative distinction between supervised infrastructure and a website.

ForecastEx, a subsidiary of Interactive Brokers that received CFTC DCM and DCO registration, extends this architecture into explicitly macro, economic, and climate domains. Its contracts cover economic indicators, central bank decisions, sovereign debt, and climate outcomes. Where Kalshi’s volume is dominated by sports — 80% of total trading volume since July 2024 — ForecastEx concentrates institutional flow in macro and central bank contracts, providing deeper liquidity precisely where signal quality matters most for risk management.

What the prices actually mean: the calibration problem

Once you accept that event contracts can exist inside serious architecture, the next question is what the prices mean. A 60-cent contract is commonly interpreted as a 60% probability of the underlying event occurring. Whether that interpretation is warranted depends on a property called calibration: whether a market’s stated probability corresponds to actual event frequencies.

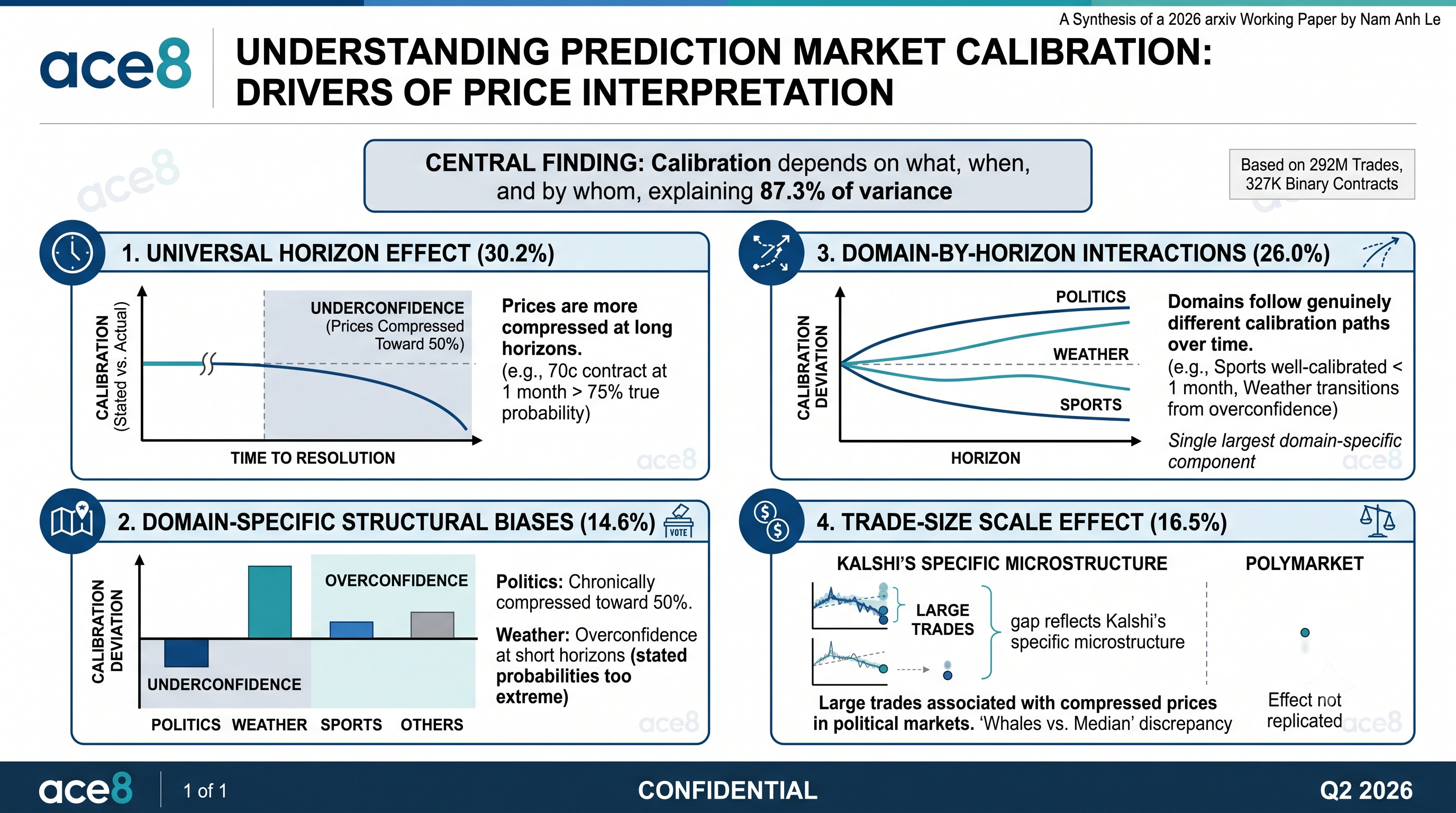

A 2026 working paper published on arXiv by Nam Anh Le decomposed calibration across 292 million trades and 327,000 binary contracts on Kalshi and Polymarket, covering six knowledge domains. The paper’s central finding is that calibration is not a domain-agnostic property of the aggregation mechanism. It depends, in structured and predictable ways, on what is being predicted, when, and by whom.

Four components explain 87.3% of calibration variance. A universal horizon effect accounts for 30.2%: all domains become more underconfident — prices more compressed toward 50% — at long time horizons, so a 70-cent contract one month from resolution corresponds to a true probability closer to 75%. Domain-specific structural biases account for 14.6%: politics is the clear outlier, with prices chronically compressed toward 50% at nearly all horizons, while weather markets display the opposite pattern — overconfidence at short horizons, where stated probabilities are too extreme relative to actual frequencies. Domain-by-horizon interactions, the single largest domain-specific component at 26.0%, describe how domains follow genuinely different calibration trajectories: sports contracts are well calibrated at short-to-medium horizons but become sharply underconfident beyond one month, while weather contracts transition from overconfidence to underconfidence as the horizon lengthens. A trade-size scale effect, accounting for 16.5% of variance, shows that in political markets, large trades are associated with more compressed prices, a gap that does not replicate on Polymarket, suggesting it reflects Kalshi’s specific microstructure rather than a universal property of political prediction markets.

The practical implication is precise. A journalist who reports that a prediction market shows “62% probability” of a candidate winning, without specifying domain and horizon, is reporting a number that requires calibration-aware interpretation to be useful. An AI system, risk engine, or executive dashboard that ingests event prices as raw probability inputs will be systematically miscalibrated, and the direction of that miscalibration will depend on what is being predicted and when. Political contracts at long horizons understate the probability of the favoured outcome; short-horizon weather contracts overstate it; sports contracts at short-to-medium horizons are relatively reliable. Organizations that build durable advantages from prediction market data will be the ones that encode this structure into their models, not those that treat market prices as ground truth.

The structural distinction between a bookmaker and a prediction market lives here. A bookmaker sets odds designed to guarantee a margin; the numbers encode the house’s risk management. A prediction market clears a price through the interaction of participants willing to stake capital; the number encodes the current aggregate judgment of those actors. That price can be read by parties who never trade. It can feed into models, hedging strategies, and decisions made by institutions far removed from the trading screen. That is the mechanism that transfers from Lloyd’s and Chicago into event contracts, and it is the mechanism the gambling narrative systematically obscures.

Blockchain, settlement, and what transfers from the platform thesis

Andreessen’s 2014 argument that Bitcoin solves the Byzantine Generals Problem — establishing trust between unrelated parties without a central intermediary — is an engineering claim about settlement infrastructure, not a claim about speculative token appreciation. A decade of crypto speculation has made it difficult to hold those two ideas separately, but for the purposes of event markets and risk instruments, separating them is necessary.3

The properties of distributed ledger technology that matter for serious event contract settlement are narrow. An immutable, auditable record of contract execution, visible to supervisors and counterparties and stored in a form that cannot be retroactively altered. Automated settlement triggered by verified external outcomes, without requiring a manual clearing operation that introduces latency and institutional counterparty risk. Reduced exposure to the solvency risk that arises when settlement depends on a single clearing institution operating opaquely. These properties, under the identity verification, surveillance obligations, and conduct rules imposed by a DCM framework, can make the settlement layer more reliable and legible than the batch-driven back-office operations that still characterize many legacy exchanges.

What does not transfer is anonymity, pseudonymous participation, permissionless access, and speculative token dynamics. Those properties follow from deliberate design choices in permissionless blockchain architectures and are not incidental to them; they are also largely orthogonal to what makes distributed ledgers useful for regulated event contract settlement. The CFTC framework is precisely what imposes the identity verification and surveillance obligations that distinguish legitimate settlement infrastructure from unregulated crypto gambling. It is the regulatory architecture, not the cryptographic substrate, that makes the technology socially acceptable.

Andreessen’s 2026 observation — that AI agents will require programmable money and that the convergence of AI and crypto is the next major structural development — adds a third dimension to this picture. Event contract prices generated under calibrated, supervised market conditions, settled via smart-contract logic on a governed ledger, and consumed as inputs by autonomous AI agents operating in real time: this is the architecture toward which the stack is moving. The organizations that understand each layer separately, and that can evaluate the governance conditions under which each layer becomes trustworthy, will be better positioned than those who respond to the entire category with either undifferentiated enthusiasm or undifferentiated dismissal.6

Climate risk, reinsurance, and the social function worth protecting

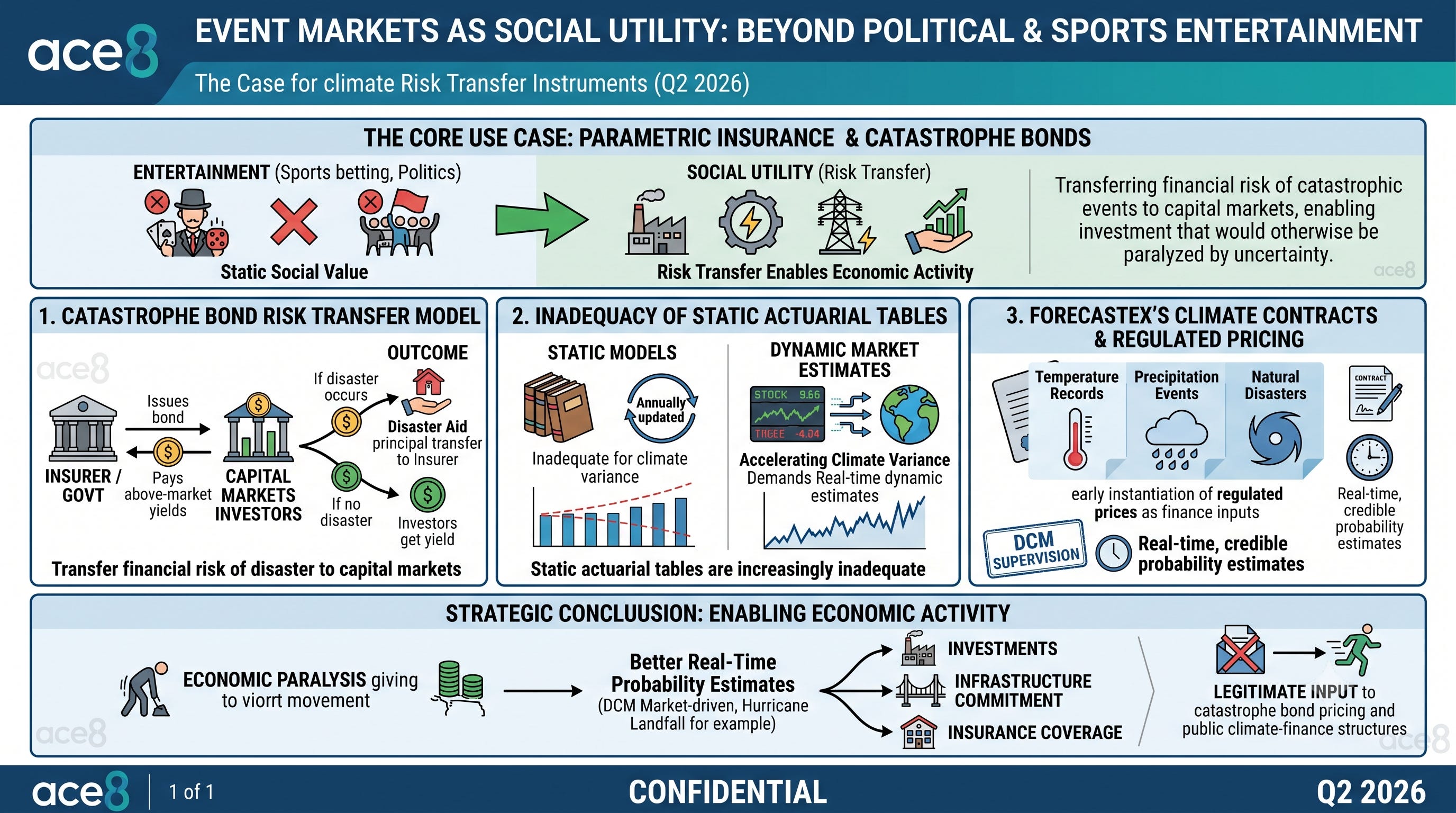

The domains where event markets carry the strongest case for social utility are precisely the ones furthest from sports betting and political entertainment. Parametric insurance and catastrophe bonds are the clearest examples. A catastrophe bond allows an insurer or government to transfer the financial risk of a natural disaster to capital markets: investors accept the risk of losing principal if a defined catastrophic event occurs, in exchange for above-market yields during non-occurrence periods. The pricing of these instruments depends on real-time, credible probability estimates of triggering events. Static actuarial tables, updated on annual or multi-year cycles, are increasingly inadequate for that function in a climate environment characterized by accelerating variance.

ForecastEx’s climate contracts — covering temperature records, precipitation events, and natural disasters — are one early instantiation of the possibility that regulated event prices can serve as inputs to instruments financing real climate risk exposure. If a hurricane landfall market operating under DCM supervision produces better real-time probability estimates than available from existing models alone, it becomes a legitimate input to catastrophe bond pricing and public climate-finance structures. The social function being served is not entertainment; it is risk transfer, enabling economic activity — investment, infrastructure commitment, insurance coverage — that would otherwise be paralyzed by uncertainty.

The calibration evidence matters here. Short-horizon weather markets are overconfident; the stated probabilities are too extreme relative to actual frequencies. That finding is not a reason to dismiss weather event markets as inputs; it is a specification of exactly how to correct for their characteristic bias. An insurer or multilateral institution that encodes domain-specific calibration structure into its use of event prices is better positioned than one that either ignores them or treats them as unbiased. This is the normal discipline applied to any noisy but information-rich data source.

The blockchain settlement layer adds operational value precisely in these high-stakes, multi-party instruments. A catastrophe bond that settles automatically when a verified physical parameter — wind speed, rainfall, earthquake magnitude — crosses a defined threshold removes the claims-adjustment friction that has historically delayed payouts after disasters, often at the cost of the people most in need of rapid disbursement. Smart-contract settlement under CFTC surveillance and identity requirements is the modern equivalent of the institutional architecture that made Lloyd’s trustworthy: not a replacement for governance, but a more efficient substrate on which governance can operate.

Key takeaways

The first is architectural. Event contracts belong in an organization’s risk and AI stack when they emerge from markets structured like Lloyd’s after incorporation and the CBOT after standardization: identity, capital requirements, surveillance, enforcement. Anything less is the long plastic hallway Thompson described. Anything with those properties is infrastructure.

The second is calibration. A single probability number from a prediction market is not a fact. It is a domain-specific, horizon-specific signal with characteristic and measurable bias. Weather markets at short horizons overstate confidence; political markets at nearly all horizons understate it; sports markets at short-to-medium horizons are relatively reliable. Any AI system, risk engine, or executive dashboard that does not encode this structure will systematically misread the signal.16

The third is about the convergence thesis. Andreessen’s 2026 claim — that AI agents will need programmable money and that the convergence of AI and crypto is structural, not speculative — is not a token promotion. It is an engineering observation about what happens when autonomous systems need to make commitments and exchange value in real time. Organizations that can separate the governance layer from the hype layer, and build toward the former while declining the latter, will have a durable advantage over those who respond to the entire category with a single gesture in either direction.6

The North Star is visible. It is a settlement substrate more transparent and programmable than current back offices, operating under governance frameworks that understand both cryptography and regulation, feeding event prices into AI systems and risk instruments that are calibrated, owned, and auditable. Getting there requires treating each layer on its own terms: the market architecture, the calibration evidence, and the settlement infrastructure as distinct problems with distinct answers.

The coffeehouse was always there. What made it matter was the architecture that came after.

References

The music business is a cruel and shallow money... - Goodreads - Hunter S. Thompson — ‘The music business is a cruel and shallow money trench, a long plastic hallway...

The quote that Hunter S. Thompson never said... - TalkBass.com - Thompson: “The Music Business is a cruel and shallow money trench, a long plastic hallway where thie...

Why Bitcoin Matters | Andreessen Horowitz - Bitcoin is a classic network effect, a positive feedback loop. The more people who use Bitcoin, the ...

Why Bitcoin Matters - The New York Times - DealBook - Bitcoin is a classic network effect, a positive feedback loop. The more people who use Bitcoin, the ...

Venture Capitalist Marc Andreessen: ‘The Grand Unification Of AI ... - Venture Capitalist Marc Andreessen: ‘The Grand Unification Of AI And Crypto Is About To Happen’. Oop...

Marc Andreessen “It’s now obvious that AI agents are going to need ... - “The grand unification of AI and crypto is about to happen.” ... “It’s now obvious that AI agents ar...

The economics of the Kalshi prediction market | CEPR - We analyse over 300,000 contracts and their outcomes, obtained from Kalshi’s application programming...

Digital Asset Exchange Receives CFTC Approval For US | Sheppard - Building on this foundation, in 2021, Kalshi, Inc. became the first fully regulated U.S. prediction ...

How are prediction markets regulated? | Market Integrity Hub - Kalshi - Learn about CFTC oversight, DCM requirements, and the regulatory framework governing prediction mark...

Industry Filings: Designated Contract Markets (DCM) | CFTC - Understanding Prediction Markets and Event Contracts · Check Registration ... Kalshi, Designated, 11...

KalshiEX LLC v. CFTC, No. 24-5205 (D.C. Cir. 2024) - Justia Law - The US District Court for the District of Columbia ruled in favor of Kalshi, finding that the CFTC e...

Know the Outcome? Don’t Trade: CFTC Puts Prediction Markets on ... - [4] Kalshi investigated the conduct quickly, and the Candidate “acknowledged that he knew these trad...

Trading volume on prediction markets has soared in recent months - Sports has made up 80% of total trading volume on Kalshi and 39% on Polymarket since July 2024. Cryp...

ForecastEx Review (June 2026): IBKR Spinout, $0 Maker Tested - ForecastEx publishes the official $0.01 to $0.99 trading band on its homepage at forecastex.com, whi...

About ForecastEx - ForecastEx is the CFTC registered Designated Contract Market (DCM) and Derivative Clearing Organizat...

Domain-Specific Calibration Dynamics in Prediction Markets ... - arXiv - Using 292 million trades across 327,000 binary contracts spanning six knowledge domains on two major...

ForecastEx - Predict upcoming events with ForecastEx. Forecast Contracts let you tap into crowd wisdom to answer ...