The Gravity of Good Enough

On Gresham’s inescapability, the black hole’s event horizon, and the man who shorted the thing that makes the thing

“Frontier AI tokens are fungible across a large and growing set of cognitive tasks — in any domain where two tokens generate equivalent alpha, rational actors will always choose the cheaper one.”

— Mark Pesce, Gresham’s Law and the Fungibility of Tokens, The Watershed, April 2026“The closer we move toward the ‘massive object’ of machine intelligence, the more our sense of time and prediction distorts, and the less our inherited strategic tools apply.”

— Alan Eyzaguirre, The Infinite Dawn, ace8.substack.com, January 2026

There is a peculiar quality to the moments when two independent analytical frames, developed in isolation, arrive at the same boundary condition from different directions. Kepler and Newton did not correspond before Newton’s laws explained Kepler’s orbits. The consilience itself was the signal — two different probes, dropped from different altitudes, reporting identical readings from the same location.

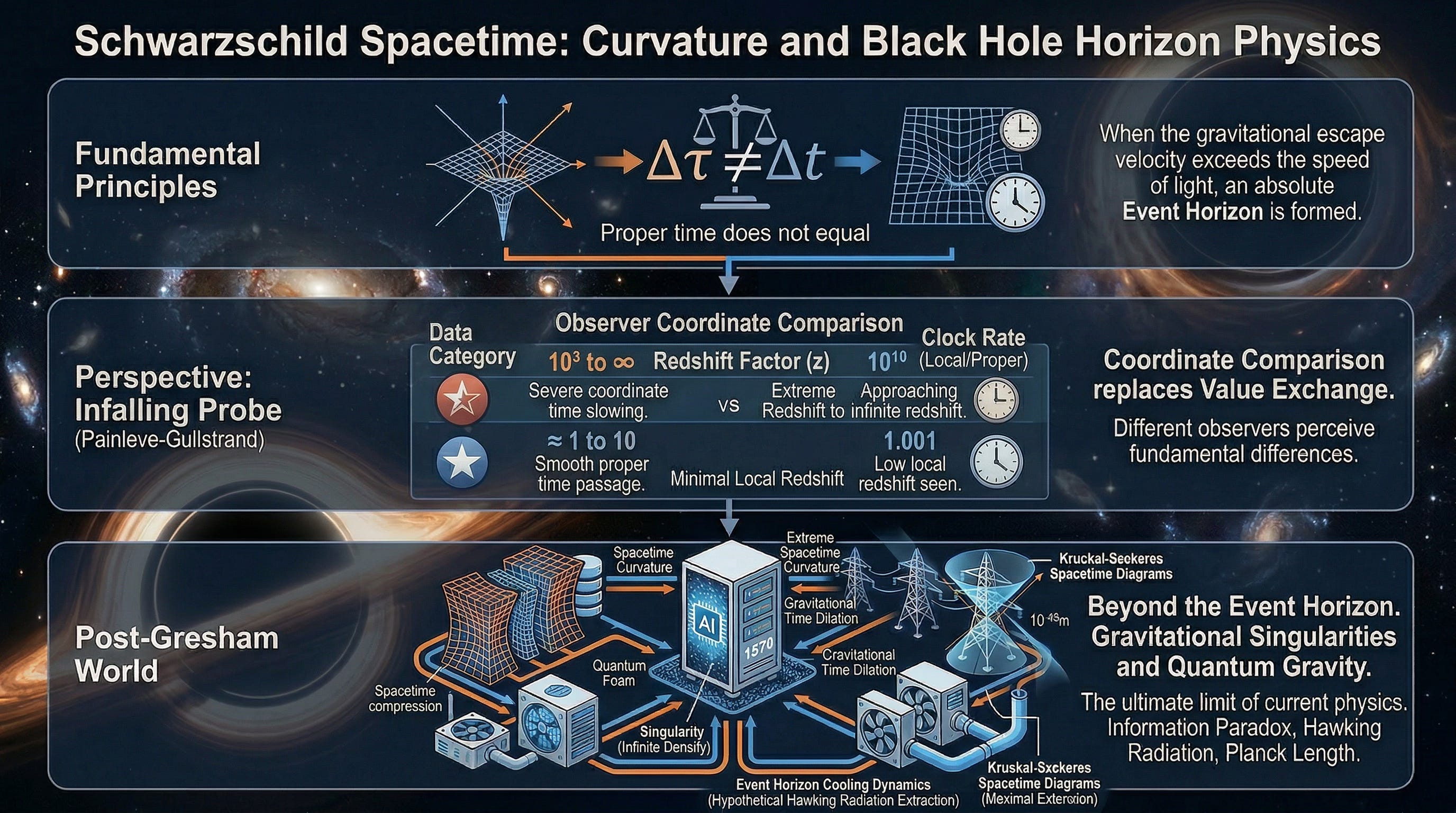

Mark Pesce’s Gresham’s Law and the Fungibility of Tokens and the black hole framework developed in The Infinite Dawnare two such probes. Pesce approached the frontier AI economy as an economist reading a currency crisis: the coexistence of expensive tokens and cheap tokens in a market that must, by Gresham’s arithmetic, resolve in favor of the cheaper one. The Infinite Dawn approached the same terrain as a physicist reading a gravitational field: the event horizon as the structural boundary beyond which normal forecasting tools cease to function, where the infalling observer’s local time proceeds normally even as the external universe accelerates away. Different instruments. Same reading. The boundary condition they are both describing is not a trend. It is a phase transition — the moment when “good enough” stops being a qualifier and becomes, simply, the market.

What neither essay could fully anticipate, because the physical world occasionally collaborates with theoretical frameworks in ways that feel almost editorial, is that the economics of compute — the infrastructure layer on which Pesce’s token mints and the black hole’s gravity well both ultimately rest — would encounter its own event horizon in the form of a war neither model had included as a variable.

The Inescapability

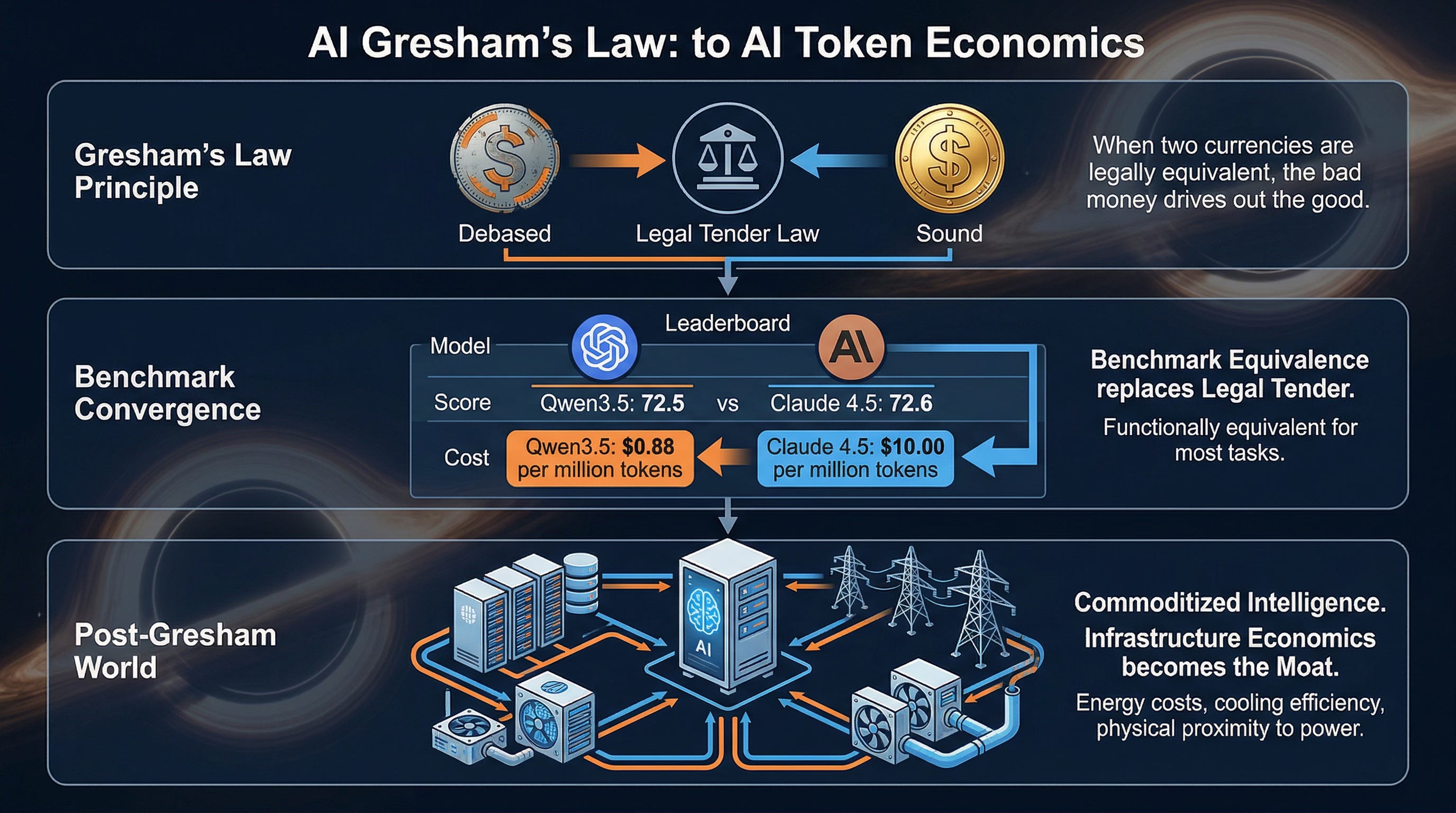

Gresham’s original observation was not primarily a comment on quality. It was a comment on legal equivalence. The law operates specifically in conditions where two currencies — the debased and the sound — are required to be accepted at face value, at equal denomination, regardless of their actual metal content. In such a condition, the rational actor does not choose the cheap coin because she prefers it. She chooses it because the market’s rules make both coins interchangeable, and holding the sound coin costs her the difference in intrinsic value without any compensating benefit. Gresham’s Law is, at its core, a description of what happens to quality when the pricing mechanism is prevented from reflecting it.

Pesce’s insight is that the AI token market has constructed this condition voluntarily. The benchmark convergence documented in the leaderboards is not merely a technical observation. It is the mechanism by which the market’s pricing rules are being reset. When Qwen3.5-397B-A17B achieves a 72.5 mean score across 44 benchmarks against Claude 4.5 Opus’s 72.6, at a blended cost of $0.88 versus $10.00 per million tokens, the market does not need to be told that the expensive token is overpriced. The market is being told, by the benchmark table itself, that the tokens are functionally equivalent for the overwhelming majority of cognitive tasks. Legal tender law is being replaced by leaderboard equivalence. The mechanism is identical. The outcome is predetermined.

What makes this more than a tactical pricing observation is the structural endpoint that Pesce identifies: “massive demand for commodity mints serving open-weight models on cheap infrastructure while confining frontier labs to a shrinking luxury market”. This is the post-Gresham world — not the moment of demonetization, but the settled state that follows it. The winners in this world are determined not by model quality but by infrastructure economics: energy costs, cooling efficiency, physical proximity to power generation, supply chain resilience. The intelligence layer commoditizes. The physical plant becomes the moat.

This is, as The Infinite Dawn observed, exactly what a black hole’s event horizon predicts. At sufficient gravitational density, local measurements become unreliable guides to the structure of the surrounding space. The benchmarks — the equivalent of local measurements — look like stable ground right up to the moment of crossing. The event horizon is not experienced as a dramatic transition from the infaller’s perspective. It is recognized, if at all, only in retrospect, from the outside, by an observer far enough from the gravity well to see the redshift.

The Short

In Q3 2025, Michael Burry’s Scion Asset Management filed $912 million in put options on Palantir and $186.6 million in put options on Nvidia. The market characterized this as “Big Short 2.0” — a contrarian bet against the AI boom made by the man who correctly bet against the housing market in 2006. By February 2026, the Palantir position was up 35%, the stock having cratered from its November 2025 high of $207. Burry posted a technical chart identifying a head-and-shoulders formation, projecting a further 40-60% decline, with a target landing area slightly above $50.

The Nvidia position, with puts struck at $110 expiring December 2027, remained underwater as of February. This distinction matters, because it suggests that Burry’s thesis is not, or not only, a bet against the AI boom in aggregate. It is a more specific structural argument — one that the Gresham framework and the black hole framework both, independently, support.

Palantir’s value proposition is, at its core, a premium-token argument: that its AIP platform, wrapping frontier model access inside enterprise-grade orchestration and compliance infrastructure, can sustain a $40 price-to-sales multiple because the software layer above the model is where durable enterprise value resides. Burry’s 10,000-word Substack essay argued that this thesis fails precisely because the software layer doesn’t reside above the model in any durable sense — that Palantir’s AIP relies on third-party model providers whose quality advantages are eroding, and that once the enterprise market internalizes the Gresham reality, the premium that Palantir charges for its orchestration layer becomes the same luxury market premium that Pesce predicts will confine frontier labs to the margins.

Nvidia’s position is structurally different, and Burry’s less-confident put there reflects this. The Gresham argument commoditizes the intelligence layer. The physical infrastructure layer — the silicon, the memory bandwidth, the packaging — is the competitive terrain that Pesce identifies as the post-Watershed advantage. If frontier tokens are commoditizing while the “good enough” market explodes in volume, then the demand for compute does not necessarily decline. It transforms: from a demand for the most powerful compute to a demand for the most economical compute at scale. Nvidia’s threat is not that demand disappears. It is that the architecture optimized for H100-class frontier training is not the same architecture optimized for commodity inference at volume. The risk is obsolescence, not irrelevance.

But then the Strait of Hormuz closed.

The Tipping Point

On the day Iranian missiles incapacitated the Ras Laffan Industrial City — the largest single helium production site on Earth, accounting for approximately one-third of global supply — the AI infrastructure thesis encountered a variable that no economic model of token fungibility had incorporated.

Helium is not a commodity that appears frequently in AI investment theses. It is not a headline input cost. It is, in the way that all critical single-point dependencies are invisible until they aren’t, simply the gas that makes semiconductor manufacturing possible at advanced nodes: the cooling medium in photolithography tools, the purge gas in EUV systems, the detection medium for vacuum leak identification, the thermal management layer in the MRI systems that happen to share supply chain prioritization with chip fabs. Its properties — extreme chemical inertness, the highest thermal conductivity of any gas, an atomic radius small enough to detect vanishingly small leaks — are not replicable by substitution. There is no helium equivalent. There is only helium.

Qatar’s three helium plants, all operating as a byproduct of LNG production, suspended operations when the Strait of Hormuz closed. The math was initially presented as manageable: a 30% loss of global capacity offset by a 15% supply overhang, netting approximately 15% shortage. But helium in cryogenic containers has an effective shelf life of 35 to 48 days before it escapes. The supply buffer is not a reservoir. It is a countdown. South Korea’s chipmakers — the primary producers of the HBM memory that powers Nvidia’s H100 and B200 architectures — held approximately six months of inventory, as of March. Six months is not long when no one knows when the Strait reopens.

The Forbes analysis identified this with appropriate precision: South Korea imported 64% of its helium from Qatar in 2025. TSMC, which had already sold out its CoWoS advanced packaging capacity through 2026, stated it was “monitoring the situation closely”. Spot helium prices surged 40-100% within weeks of the conflict’s beginning. Bank of America’s supply chain report characterized the situation as “supply-constrained, not demand-constrained” — which is precisely the wrong constraint at the wrong moment for an industry whose entire investment thesis has been premised on demand being the binding variable.

The J.P. Morgan asset management analysis observed that “business cases for AI investment will likely narrow to focus on AI workloads that originate in the region and benefit consumers and businesses” if extended conflict drives sustained cost increases through the supply chain. This is diplomatic language for a structural repricing of the infrastructure economics that underpin every AI investment thesis currently circulating.

Now follow the Gresham logic through this physical constraint.

The premium frontier model was already losing its pricing justification to the commodity model on performance grounds. The commodity model wins, Pesce argues, by controlling “physical infrastructure advantages” — cheap power, cheap cooling, optimized inference architecture. But “cheap infrastructure” is a relative term that becomes meaningfully less stable when the gas required to manufacture the chips that power the infrastructure becomes a strategic commodity subject to Middle Eastern geopolitics. The Gresham race to the bottom in token pricing has been predicated on the assumption that compute costs would continue their historical decline curve. The Iran compute shock introduces a scenario where that curve inverts — not permanently, not catastrophically, but sufficiently to alter the math at the margin that matters most.

The companies that will survive this inversion are not the ones with the best models. They are the ones with the most resilient supply chains, the deepest helium hedges, the fastest capacity to route production to facilities with alternative sourcing — TSMC’s Arizona fabs, which draw on North American helium from Wyoming and Kansas; Intel’s facilities with diversified supply arrangements; the hyperscalers large enough to have negotiated multi-year helium contracts before the conflict began. Nvidia’s long-term position in this environment is not simply a bet on continued frontier training demand. It is a bet that the physical infrastructure for frontier compute will remain accessible at the costs baked into current forward earnings multiples. Burry’s $110 December 2027 put, which seemed pessimistic against a $187 stock, is now being stress-tested by variables that had nothing to do with his original thesis and validate its structural logic anyway.scientificamerican+2

The Convergence

The black hole framework’s most useful property is that it explains why these three dynamics — Gresham’s token commoditization, Burry’s infrastructure fragility thesis, and the Iran helium supply shock — feel as though they arrived simultaneously rather than sequentially. They did not arrive simultaneously. They were already converging. The event horizon was already present. The experiences of gravitational time dilation that The Infinite Dawn described — visibility windows compressing from eighteen months to three to six months, long-range planning collapsing into stance — are the phenomenology of approaching an event horizon, where multiple causal threads, developing at different rates across different domains, appear to an inside observer as a sudden cascade.

The cascade is not a cascade. It is an arrival. The observer has been falling for some time. The horizon was always there.

What Pesce’s Gresham analysis contributes to this frame is the mechanism by which the post-event-horizon world is structured. Once the pricing equivalence of tokens is established — once the leaderboard compression makes the market’s Gresham logic operational — the competitive terrain shifts entirely to infrastructure economics. The model quality race ends not in a winner but in a floor: a “good enough” threshold below which no serious production use case bothers to go, and above which premium pricing becomes, in Pesce’s term, a “luxury market.” What the Iran supply shock reveals is that the infrastructure economics that Pesce identifies as the new competitive terrain are themselves not stable — that the physical plant, which was supposed to be the secure foundation after the intelligence layer commoditized, has its own event horizon: the point at which the supply chain assumptions that made cheap inference economics possible cease to hold.

Burry positioned himself not as a prophet but as a diagnostician. His framing — a “fragility diagnosis” rather than a date prediction — is the correct epistemic register for this moment. He is not calling the crash. He is identifying the structural preconditions under which a small shock triggers fast drawdowns in a system whose valuation multiples have been calibrated for a world of continuous cost decline and uninterrupted supply. The Iran war did not create the fragility. It found it, the way seismic activity finds a fault line that was always there.

The Inescapable Remainder

Gresham’s Law has an endpoint that is sometimes overlooked in summaries of the principle. The bad money does not simply circulate while the good money is hoarded. Eventually — when the debasement becomes severe enough, or the legal tender fiction becomes unsustainable enough — the currency system undergoes revaluation. The bad money, having driven out the good, then faces its own reckoning: it is no longer backed by the good money it displaced, and its value is revealed to be exactly what the market always knew it was. The circulating medium re-prices to reflect reality.

In token economics, this revaluation has not yet occurred. The “good enough” frontier is still being established, the commodity mints are still scaling, and the premium labs are still commanding price points that the benchmark table suggests will become increasingly difficult to defend. The Iran compute shock is not the revaluation. It is the friction that reveals the mechanism — the moment when the infrastructure layer, which was supposed to be the stable ground after the intelligence layer commoditized, is shown to have its own Gresham problem: when cheap power and cheap chips are revealed to depend on supply chains routed through a chokepoint that can be closed by a drone attack on a Qatari LNG facility.

Burry is not warning that AI will fail. He is observing that the specific financial instruments built on the assumption of AI’s unconstrained success have been priced as though the event horizon doesn’t exist — as though the convergence of token commoditization, infrastructure fragility, and geopolitical supply risk is either individually manageable or simply not present in the frame.

The black hole, The Infinite Dawn noted, does not announce itself. The event horizon is identified by its effects on the things surrounding it — the redshifting of light, the distortion of time, the impossibility of escape beyond a certain radius. The convergence of Pesce’s Gresham mechanism, the Iran helium shock, and Burry’s fragility diagnosis is not three separate stories. It is one event, viewed from three different instruments. The reading is consistent. The location is now.

Alan Eyzaguirre writes about technology, industry structure, and the long arcs that connect them. ace8.substack.com.